I am an aspiring finance professional, Chartered Accountant qualified in May 2015 and also a B.Com graduate from Allahabad University batch of 2011. I have 3.5 years of post qualification working experience in Accounting and Tax.

Finance, accounting, taxonomy is continuously changing with the digital disruption happening around the world. The ABC of technology – Data Analytics, Blockchain and Cloud Computing is changing the way accounting operations and businesses are handled in organisations nowadays. In order to match up we need to be abreast with these changes and keep us updated to be successful in our careers.

I am creating this blog to pen down my thoughts and share my knowledge and expertise on subject matter in areas of Accounting, Tax, Laws and Technology. I have always wanted to become a writer and speaker, so this will be my first step towards fulfilling my dream. I am still learning everyday and here I will like my followers to learn and grow with my experience and share there knowledge as-well.

If you have any thoughts, please write down to me and we can share it on this platform. I will appreciate suggestions and feedback. Good luck.

We all started there with the dream to make a big name for us, a name of repute, a name which in itself is a denomination of success, we worked hard day and night to earn those 2 golden words in front of our name “Chartered Accountant”. But alas! even after putting so much effort, studying day and night, sacrificing those friends, festivals, relationships, could not clear the exams!

Now you have either completed your articleship and appearing for Final exams or you are still stuck in the loop of IPCC exams and can not even begin articleship making the entire CA course even longer for you. You feel entrapped in the vicious circle of attempt after attempt or November after May and then November again and can not understand why life is taking a toll on you. The number of attempts is not leading you anywhere and you don’t see any silver lining in your mark-sheet, you have tried all the different methods of study-plan and still not getting success.

See, time is ticking, life is moving fast around you, you can see your friends graduating, taking up jobs, and even getting married. Not only that the world around is fast-paced, governments shifts, change in way of doing business leading to thrust in the adoption of new economic policies, amendments in existing laws and changes in accounting standards, etc. Hence, what you studied while starting the course has become redundant and a new syllabus has been applied.Now it is for you to think and take action that even if 4-5 or more years of only studying for CA exams has not led you anywhere and you are not getting the desired results, it’s time to change your mindset and explore other areas! Do something different, take a break, and try other areas in life. Try another lens, look at your career options from another angle, if something is not working for you, there will be 10 more things you can thrive at. The world is big out there and you need to see outside the box and find something that can work for you.

To suggest, there are plenty of accounting courses out there that don’t take as much time to complete but stand at par with CA. To name a few is CMA, CPA US, ICMAI, ACCA, CFA, Company Secretary, LLB and the lists goes on. If you can’t afford to take a course again, take up a job backing your experience and knowledge so far and simultaneously work for some other accounting degree recognition. Remember no degree or course can give you success, it is just validation for your skills and knowledge. Chartered Accountancy is no doubt an esteemed degree, most sought after when you go for employment in India, it can give you a good salary to start with but it can’t guarantee your success in the long run. Only your attitude, skills, knowledge, and the ability to apply them in your day-to-day life will help you climb the ladder of success. I have seen people in top positions without having that big fancy degree or college name and still shining bright. Also, I have seen people who after getting the CA degree are no more working in the related field and have chosen altogether a different career path for themselves.

Trust life is big and it’s foolish to be doing something for so long which is not yielding results for you. As Albert Einstein has rightly said, “Everybody is a genius but if you judge a fish by its ability to climb a tree, it will live its whole life believing that it is stupid”. Hence be flexible in life, you may have started with a career path to begin with but if it is not fruitful, be wise enough to make a decision before it’s too late. If you are struggling to make a decision, talk to your elders, friends, colleagues, you can also reach me through a personal message and I will be happy to guide you. With this, I will like to close, wish you success and happiness.

As I am writing this article, there is an exponential rise in the number of Coronavirus cases all over the world, there is barely a country unaffected by this virus. USA has surpassed China w.r.t total number of deaths due to Virus & is nearing 200k mark in the total number of cases. The White House has projected today that total deaths in USA can rise to at least 240000. Italy, Spain have taken the worst hit and now the virus is multiplying in India, affecting not only those contracted with the virus but also the poor who can’t earn their bread anymore due to lockdown and are forced to move back to villages.

Health ministries are predicting that at least 70% of the world population will be infected by the COVID-19 and the Pandemic will take another 2 years to run its course. Seeing the number of deaths reported everyday on News and the world not able to contain the virus or come with a vaccine soon, one can predict that global population may see sharp fall and some even recovered from the disease will be disabled by after-effects. Only those who will pass Darwin’s Survival of the Fittest theory will rise as survivors and will be responsible for running the world.

The world after Pandemic will be in healing state – will compete again for economic growth, industrial production, infrastructure development. The necessity for upgrading medical systems of the countries will be prioritised and many medical colleges will open; simultaneously will emerge the need for boosting IT infrastructure. The markets will start performing as before and demand for goods and services will pick up. Government and organisations will start hiring again for new opportunities created and demand to fulfil various vacant positions will arise, not only for new jobs but also for the jobs the predecessors of whose have deceased during the epidemic. We will need more doctors, engineers, economists, administrators, teachers, NGO’s, etc. to bring the world back to its original position.

With this will come abundant opportunities for those who have survived, stayed at home and have also worked on upgrading their skills. You will be open to grab more jobs and your suitability may increase for various positions for which you were not experienced earlier. More jobs will also be created in countries which are worst affected by it as they will need a working community to support their growth and one can see more import of talent in these countries in coming years. So this might be an opportunity in adversary for many those who wanted to grow in their career paths or wanted to pursue some different field. You have the time now, start working towards it. Make the best use of time home and upgrade your skills to match that dream role.

We can see other changes as well – the rise of another Superpower; the concurrence of the world to Sustainable economic development; rise and fall of various industries; changes in the way we do business today, the way we work in offices and need to commute to work or for businesses around the world. Various new laws will be enacted dealing with Outbreak situation and restricting the movement of people across countries. School syllabuses and the world basic hygiene rules will undergo change once again.

So dear readers, let me know your thoughts about how the world will look after Pandemic and how soon you think Life will be normal again. Will more job opportunities will be created or reduce. Please comment, what we can do to deal with this or what unique things you are doing home this lockdown. I wish you all good health and safe environment.

Big 4 interviews like any other interviews generally start with basic introduction of the interviewer and then for yourself, this is generally done so you can get relaxed and become warm with the interview environment. While answering this it is best to focus on your qualification, previous work experiences and types of audit handled.

Few frequently asked interview questions and there best answers are given as below:-

1. What do you understand by external Audit?

External audit is an independentexamination of financial statements of an entity for the purpose of expressing an opinion whether the financial statements are prepared in all material respects in accordance with the applicable Financial reporting framework andgive a reasonable assurance that they are free from any material misstatements due to error and fraud.

2. What do you mean by absolute assurance and reasonable assurance ?

Absolute meansabsolutely sure, An absolute assurance will mean that there is absolutely no misstatement in the financial statement and thus financial statements are absolutely reliable and relevant for the user of financial statements. On the other hand reasonable assurance is also a high level of assurance but it means that auditor has conducted the engagement in a way that he is reasonably i.e. to the best possible extent provided the situation circumstances he is reasonable sure that financial statements are free from material misstatement but there might be some misstatements that go undetected.

3. What comprises the financial statements for a company?

A complete set of financial statements comprises of: (a) a balance sheet as at the end of the period ; (b) a statement of profit and loss for the period; (c) a statement of changes in equity for the period; (d) a statement of cash flows for the period; (e) notes, comprising significant accounting policies and other explanatory information; (f) comparative information in respect of the preceding period; and (g) a balance sheet as at the beginning of the preceding period when an entity applies an accounting policy retrospectively or makes a retrospective restatement of items in its financial statements, or when it reclassifies items in its financial statements.

4. What is included in notes to accounts?

An introduction of the business outlining its legal status, its country of incorporation and the name of its parents if any and a statement about the company’s areas of business and its operations.

A summary of accounting policies related to revenue recognition, inventories, property, plant and equipment, financial instruments, etc.

A schedule of property plant and equipment showing the addition and deletion of assets, related movement in the accumulated depreciation account and book value.

A breakup of cost of sales, selling expenses and administrative expenses.

A detailed disclosure of different classes of financial instruments and their related risks.

A breakup of the gross amounts and present values of lease obligations of the business.

A detail of transactions with related parties.

A detail of contingencies that may affect the business in future, for example legal proceedings against the business.

A description of major events that occurred after the balance sheet date, etc.

5. If you are going for audit in an organisation, what will be your approach towards audit?

The whole auditing process can generally be divided into three different phases. The audit planning phase includes procedures such as gaining an understanding of the client and its business, making risk and materiality assessments, determining an audit strategy, and determining the type of evidence to collect, based on the risk levels.

Performingtheaudit refers to the process of collecting evidence. Finally, the reporting phase deals with making conclusions, reporting any necessary adjustments to management, and issuing the audit report.

6. How do you perform sales or revenue audit?

Internal Controls: Understanding how entity has set up internal control relating to revenue recognition in terms of prices authorisation, goods or services delivery process, revenues recording process, billing and correction process.

Review the sales occurrence: This is performed by obtaining the sales transactions recorded in the financial statements during the period as well as sales report that link to the financial statements. Then perform an audit sampling to total population of those sales transactions to review against quotation, sales orders, invoices, contracts and goods delivery noted. Ensure that the sampling items are represent the total population, otherwise the conclusion might go wrong.

Perform Sales Revenues Analysis: This could help auditor to identify the unusual event or transactions related to sales. For example, comparing the sales trend again the goods of goods sold or inventories. This analysis could help auditors to perform additional review if they found that the trend go in different direction.

Review the sales price authorisation. The fraud over this area is likely to happen. Management is the one who manages and make sure that fraud risk is protected and minimise. But, auditor should also review the control over this area. Focus on unauthorised sales, and unauthorised sales commission that link to performance incentives of sales team and sales manager.

Review the collectability: Sales increase is good but collectability of those sales amount is importance. Account receivables analysis should be performed, and credit policy should be reviewed. Review the write-off amount of account receivable during the year and then assess its reasonableness.

Review the sales recognition whether the recognition of sales during the period are respecting the IAS 18 or not. It is importance to assess that the future economic related to sales will be inflow into the company and the sales amount is measurable.

Review the completeness of revenues recording in the financial statements. Revenues might be understated if they are under recorded.

7. How will you do audit of debtors?

The auditor should obtain the list of debtors duly certified by the responsible official and scrutinise for its accuracy.

He should obtain the confirmation letters of the statement of accounts directly from debtors and the same should be verified to check the actual existence of debtors. He should pay special attention to those balances for which confirmations are not available.

The sales ledger balances should be checked with the Debtor’s Ledger, Sales Book, Sales Returns Book, cash book, etc.

He should see that the book debt balances do not include the amounts due in respect of goods out on sale or return basis.

He should see that the book debts shown in the Balance sheet are recoverable.

He should obtain a duly certified statement classifying between good debts, secured debts, unsecured debts, current debts, bad and doubtful debts, and debts outstanding for a period exceeding six months.

He should see that adequate provision has been made for bad and doubtful debts.

8. How to audit trade payables?

A trade payable is an amount billed to a company by its suppliers for goods delivered to or services consumed by the company in the ordinary course of business. These billed amounts, if paid on credit, are entered in the accounts payable module of a company’s accounting software, after which they appear in the accounts payable ageing report until they are paid. Any amounts owed to suppliers that are immediately paid in cash are not considered to be trade payables, since they are no longer a liability. Processes that can be used to audit payables are:-

ExaminationofSOPs or Working Instructions for AP process and see if the company is following them.

Analysis of paper trails- Analysing this paper trail requires auditors to review original source documents, such as Purchase orders, Vendor invoices, Journal entries for AP and inventory, and Bank records.

Balance Confirmations- Auditors may send forms to the company’s vendors asking them to “confirm” the balance owed. Confirmations can either include the amount due based on the company’s accounting records, or Leave the balance blank and ask the vendor to complete it.

Verification of financial statements- Auditors compare the amounts recorded in the company financial statements to the records maintained by the AP department. This includes reviewing the month-end close process to ensure that items are posted in the correct accounting period i.e. the period in which expenses are incurred.

9. What is audit risk and what are its types?

Auditrisk refers to the risk that an auditor may issue an unqualified report due to the auditor’s failure to detect material misstatement either due to error or fraud. It is classified as inherent risk, control risk and detection risk.

10. What are fictitious assets?

Fictitious assets are the expenses or losses which are not fully written off (not offset in the Profit and Loss A/c) during particular accounting period. These expenses or losses are spread over more than one years. The part of these expenses or losses to be shown in the profit and loss account and the remaining amount will be carried forward to the following years. These remaining amount will be shown in the Balance Sheet of the company. Example advertisement expenses, discount on issue of shares and debentures.

11. What are audit assertions?

Occurrence :Transactions recognised in the financial statements have occurred and relate to the entity.

Completeness: All transactions that were supposed to be recorded have been recognised in the financial statements.

Accuracy: Transactions have been recorded accurately at their appropriate amounts.

Existence: Assets, liabilities and equity balances exist at the period end.

Cut-off: Transactions have been recognised in the correct accounting periods.

Classification: Transactions have been classified and presented fairly in the financial statements.

Rights & Obligations:

Entity has the right to ownership or use of the recognised assets, and the liabilities recognised in the financial statements represent the obligations of the entity.

Valuation: Assets, liabilities and equity balances have been valued appropriately.

12. Tell me about IFRS 16?

The IFRS 16 – is the new leases standard. It comes into effect on 1 January 2019. The new standard requires lessees to recognise nearly all leases on the balance sheet which will reflect their right to use an asset for a period of time and the associated liability for payments. It specifies how an IFRS reporter will recognise, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognise assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value. Whereas lessors continue to classify leases as operating or finance.

13. What are Deferred taxes, can you give example of each deferred tax assets and liabilities?

Deferred tax refers to the tax effect of temporary differences between accounting income that is calculated by taking into consideration the provisions of Companies Act, 2013 and taxable income that is calculated by taking into consideration the provisions of Income Tax Act,1961. Deferred tax assets are created when Book profit is less than the Taxable profit common examples are bad debts reserves, employee benefit plans, pension plan reserves, carry forward of tax losses.

Deferred tax liability is created when Book profits are higher than the Taxable profit, Eg. in case of depreciation. Generally the depreciation rate as per Income tax act is higher than the depreciation rate per companies act specially in the initial years, so entity will end up paying less taxes for the current period and this will create DTL.

14. What are your strengths and weaknesses, what are you doing to improve them?

While answering these types of questions be sure to mention the skills related to job, like you are a good learner, audit enthusiast, has good leadership and managements skills, good in automating tasks, etc. backup these with any previous references.

Questions for weaknesses are tricky ones and should be answered very carefully, don’t mention the skills that can be seen as affecting your job role. So you can say like you are little emotional, very helping nature and can’t say no., etc. Look for more examples in Google and it will help you for your preparation.

15. Do you have any team handling experience, what were the challenges faced and how you overcome it?

These is asked to understand how you can be seen as working with the team, are you a team player and can collaborate and complete tasks. How the team can synergise with your presence and contribute to achieving business objectives as a whole. Answer these with your previous experience and mention your coaching and team building skills here.

16. Any challenges and achievements in past work?

While answering such questions be to the point and briefly describe the situation and corrective actions taken for a scenario. The best way to go for it by using the SCAR method- Situation, Consequences, Action and Results. Talk about how you faced a conflict or identified a major problem in the system, how it was impacting the business, and how you resolved it in a timely manner and its results.

17. Any questions you have from me?

Always have some questions for the interviewer, try to know more about the job profile here, how it will be like working with them, how is the team, what will be the career progression with them, any training will be imparted, etc. This shows that you are genuinely interested in the job and you can ask anything in more detail which was mentioned earlier by interviewer, this will demonstrate you were listening to him/her carefully and will boost your job candidature.

I keep getting many questions from friends and peers on LinkedIn from India and Australia about my CPA Aust. Program. To answer this I am writing this article, what CPA is, why I started this program and how you can register for the same.

So, I am a qualified Indian Chartered Accountant with 3.5 years of experience in Accounting and tax in India. I recently got married and since my husband job was located in Australia, we decided to migrate there for long time and build our careers there.

Why I started this program

As soon as I moved there, I realised that job environment in Australia is not easy and you need to have local experience and good contacts to get your preferred job there. Also it is beneficial if you have a local recognised accounting degree because most employers ask for a CPA or CA ANZ for good accounting, audit or tax roles. So, I explored my options between CPA Aust. and CAANZ and decided to go for CPA Australia as it suited my requirements, also I had to go only for 1 paper- Global Strategy and Leadership(GSL) and 1 online test for Governance and Accountability.

I had attended one of the “Become A CPA Information Session” in Melbourne and there met many people like me from India, China, Sri Lanka who had migrated to Australia recently and looking for career options in accounting. I was happy to see the kind of network these platforms help you build and we were guided by qualified CPA’s and mentors already working in Australia. Here I will like to state after that I attended many workshops and seminars conducted by CPA Australia and thankful for their such inclusive knowledge sharing networks. Now I am in India and still committed to accomplishing my CPA status and here in India also I get ample opportunities to attend CPA chapters.

What is CPA Australia? taken from CPA website

CPA

Australia (“Certified Practising Accountant”) is a

professional accounting body in Australia founded

in 1886, with 164,695 members. A CPA is a finance, accounting and business

professional with a specific qualification. Being a CPA is a mark of high

professional competence. It indicates a soundness in depth, breadth and quality

of accountancy knowledge.

How to

register for it and who can benefit

The first step will be to visit the CPA website https://www.cpaaustralia.com.au/become-a-cpa and collect more information about the course, depending on your qualification whether a graduate in commerce or any other recognised Professional accounting degree you possess in India or your home country, you can get exemptions in certain examinations of CPA Program. The final level known as CPA Program has 6 papers.

The

elective subjects are:-

FINANCIAL PLANNING FUNDAMENTALS

ADVANCED TAXATION

ADVANCED AUDIT & ASSURANCE

FINANCIAL RISK MANAGEMENT

RISK ADVICE & INSURANCE

CONTEMPORARY BUSINESS ISSUES

INVESTMENT STRATEGIES

Step 1. Application to Become CPA

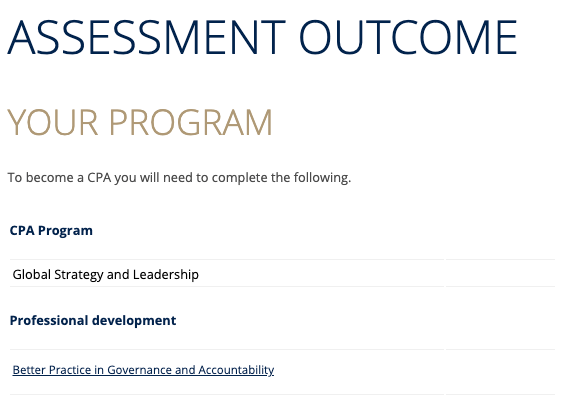

To know which subjects you are eligible for exemption you have to start with the Application process with CPA Institute, who will then share with you the assessment outcome. In the application you have to submit all your details of education, work experience and pay an application fee. Application fee is AUD 164, but you can get a promo code or something when you attend the CPA Information session in person and redeem it against application fee.

The assessment outcome may look something like this

depending upon your experience:-

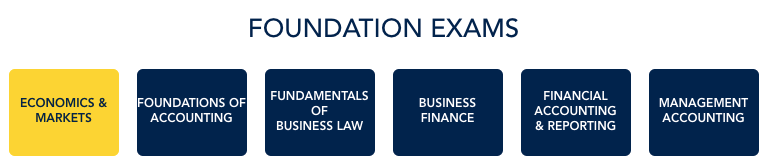

But if you

are coming altogether from a different discipline you have to start with CPA

Foundation which have 5 subjects as below:-

Step

2. Membership Fees

Unlike other professional accounting programs like Chartered Accountancy of ICAI which give you to use their name “CA” only on becoming fully qualified, CPA Aust. give membership to its students at the time of registering for the course, so you can use the words APA Aust. (Associate Practising accountant) besides your name and show your commitment to prospective employers towards your education. On completing the program you are entitle to use CPA Aust. title besides your name. Membership fees for the year is AUD 325, for half year is AUD 162.5 depending when you join the program. As a member you are eligible to access many online resources of CPA Aust. and there library. Note fees keep changing so visit https://www.cpaaustralia.com.au/member-services/fees/australia for updated details.

Step 3. Enrolling for the subject

You are enrolled for a subject or many subjects per semester, for example I enrolled for GSL paper soon after my assessment outcome. One subject enrolment will cost you around AUD 1140. After successful enrolment and payment you will receive your study material in hardcopy from CPA Institute and also many online resources to help you guide throughout your semester. To help in your studies you can also form a study groups with students enrolled for same subjects in your area. Exam are held twice a year in April/May and September/ October. Results announced a month later.

Overall my experience with the CPA Aust. was really good, I was able to connect with many people like me and also became part of ICAI chapters in Melbourne through this network. I decided to take it so that I can get local accounting body recognition as I have plans to work in Australia for long time. If you have any questions you can also reach the CPA Aust. support phone nos.: 1300737373 (within Australia) and +61 396069677 (outside of Australia). Hope this helps you in your decision to pursue the course, if you have any queries please reach me on fcasnehasingh@gmail.com.